New York, NY

Shift – the leading center of expertise on the UN Guiding Principles on Business and Human Rights – welcomes the proposal by the European Commission to amend the Non-financial Reporting Directive (NFRD) and related Directives to develop a renewed sustainability reporting regime in Europe (the Corporate Sustainability Reporting Directive, CSRD). The legislative proposal follows the report by the Project Task Force of EFRAG (EFRAG PTF), on which Shift commented in March 2021.

In addition to supporting the statement by the Alliance for Corporate Transparency, Shift highlights the following positive points and suggests where certain elements require further attention:

Double materiality

Positive development

The current NFRD offers a unique and unprecedented approach to materiality: it requires entities to report both on impacts on people and the planet by businesses, as well as on risks to the business itself. As the EFRAG PTF pointed out, it is critical that the new reporting regime provide clear direction and guidance, so that companies report not only on where impacts and risks overlap, but on the full range of sustainability impacts and risks, in line with international standards. The proposed CSRD is “removing any ambiguity” (p. 13) that this should be the case. Moreover, it makes clear that the materiality assessment should include risks and impacts across the full value chain (p. 43, among others) and that reporting entities should disclose the process that they use for determining their material issues (p. 43).

Points needing further attention

It is critical that the EU and its member states find coherence between what they are mandating companies to do on human rights and environmental due diligence (HREDD), and what they are expecting them to report on. While the explanatory memorandum of the proposal refers (p.5) to the Sustainable Corporate Governance Initiative (which is due to issue Commission proposals on mandatory HREDD this summer), the need for alignment with this forthcoming legislation should be strengthened in the CSRD itself (once the mandatory HREDD proposals are issued) if it is to be translated into the standards. This is particularly important where it relates to prioritization, and the new reporting regime should establish clear methodologies to prioritize sustainability issues under an impact materiality lens that are in line with the EU and international standards referenced in the proposal.

“Social” Issues

Positive development

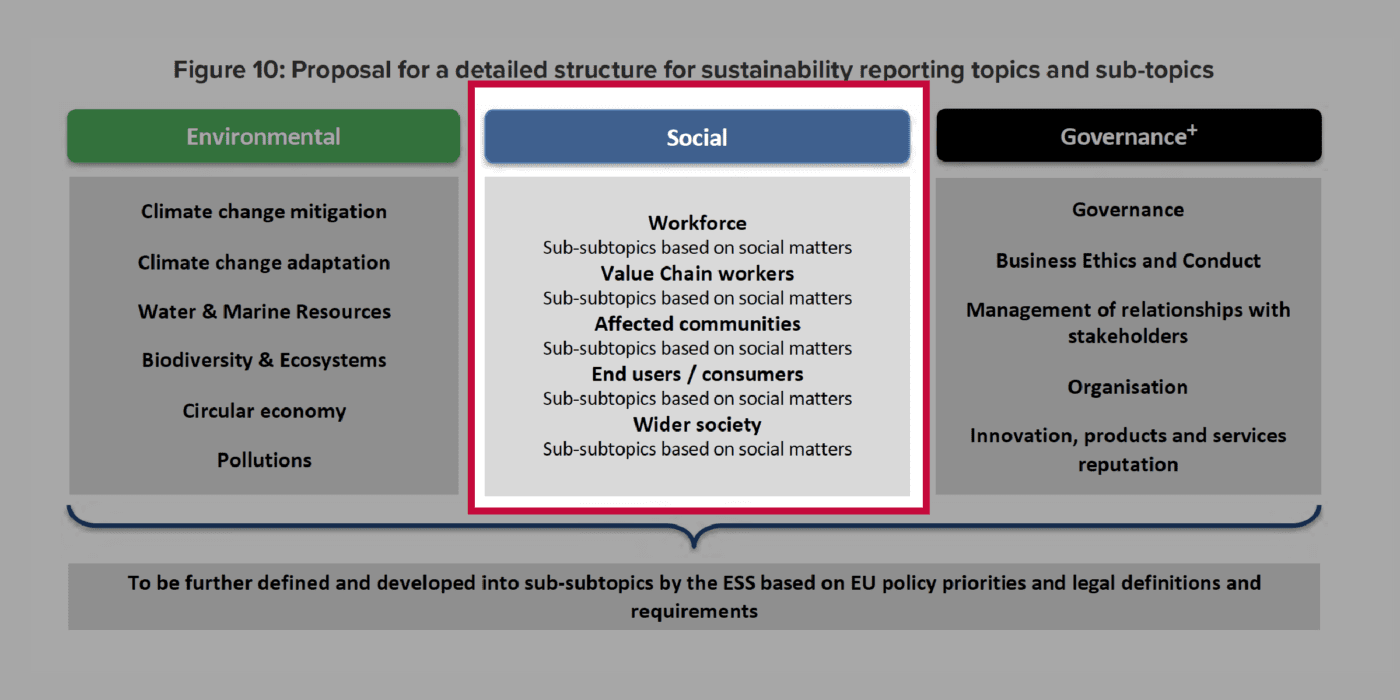

The proposed CSRD includes a new list of more detailed sustainability topics and subtopics that entities would be required to report on, organized around the three ESG pillars. The Commission did not follow GRI in re-naming the second pillar “People” rather than the often misunderstood and misrepresented category of “Social”; however, it is noteworthy that issues critical for addressing inequality and vulnerability of workers and others in company operations and value chains, will now need to be reported on by all companies. This includes:

- Equal opportunity, including related to gender, equal pay for equal work and people with disabilities;

- Working conditions, including wages, social dialogue and collective bargaining;

- Respect for human rights broadly with a reference to core international and EU standards.

The proposal also identifies several sub-topics under the “governance” pillar (e.g., lobbying activities, payment practices) that are often critical for understanding human rights performance.

Points needing further attention

While the current NFRD positions human rights in a problematic way (separating ‘social and employee matters’ as a distinct category rather than as a subset of human rights), the new proposal does not necessarily provide more clarity and structure. Shift encourages the CSRD to adopt the EFRAG PTF’s recommendation to organize the people/social pillar on the basis of who could be affected, which would provide a much-needed organizing construct: starting with the stakeholder groups that can be impacted and then articulating sub-topics for the types of impacts those people can experience. At a minimum, it should recognize that they are not abstract ‘sub-topics”, but represent impacts on actual people that need to be explicitly identified by the reporting entity in order to be appropriately managed and reported on.

EFRAG Governance

Positive development

If and when the CSRD would be adopted by the EU, EFRAG would be tasked with developing the more specific EU Sustainability Reporting Standards (level 2), building on the parameters set out in the proposed legislation (level 1). To this end, EFRAG has proposed an update of its governance, which according to the proposed CSRD, should include, “a balanced representation of experts from national authorities, civil society and the private sector,” (p. 9) and that its advice to the Commission for adopting new sustainability reporting standards should be, “developed…with the expertise of relevant stakeholders” (p. 53).

Points needing further attention

EFRAG’s traditional constituent stakeholders come from different institutional backgrounds (business, audit/assurance, investor etc) and have experience in financial reporting. Many of those same organizations have experience with financially material sustainability issues. But expertise in the material impacts of business on people and the environment, and what makes for meaningful reporting about them, often sits elsewhere. ‘Balanced representation’ therefore needs to mean more than just equal numbers from each constituency if it is to cover the very issue that makes the CSRD a holistic reporting proposition – the concept of impact materiality. Getting this right will determine whether the pioneering concept of double materiality succeeds or fails once it moves from paper to practice.

Ensuring relevant reporting

Positive development

Throughout the proposal, it is emphasized that the new sustainability reporting standards, “shall require that the information to be reported is understandable, relevant, representative, verifiable, comparable, and is represented in a faithful manner” (p. 45, emphasis added). The word “relevant” is critical here, since earlier communications around the NFRD at times overemphasized comparability (as many current reporting initiatives still do), often at the expense of ensuring relevant and meaningful reporting on people matters.

Points needing further attention

To give real substance to this criterion, the new reporting regime should build on the EFRAG PTF’s proposals that it, “should develop guidance on principles governing the quality of information”, including by setting criteria for the quality of indicators, “that test the validity of the insight the resulting information can provide to users and the potential for unintended consequences from their application” (proposal #14 & 15, p. 66-67).