Shift, together with the Capitals Coalition, has spent two years working with companies, investors, standard-setters, living wage initiatives and accounting experts to develop an accounting model for living wages to enable standardized, meaningful, and comparable reporting on progress made by companies in their own workforces and supply chains.

Efforts to tackle growing levels of inequality and poverty around the world are increasingly focused on the payment of a living wage. That’s because realizing the human right to a living wage is essential to raising the living standards of the most vulnerable workers and their families – and to fulfilling a range of other human rights, including rights to food, water, health, adequate housing, education, family life, and fair working hours.

The wider impact on society is also clear. Studies have shown that reductions in poverty and inequality can lead to greater social cohesion, as well as benefits to business. Paying a living wage can deliver not only a more motivated and productive workforce, with lower staff turnover, but also improved revenues and profits and increased value chain resilience and performance.

Measuring and reporting on living wage progress is essential to driving better outcomes for workers, businesses, and for society.

Investors are increasingly interested in whether companies are taking action on living wages, and if so, whether those actions are having any positive impact on workers’ wages. To be able to make an informed assessment of this aspect of a company’s performance, investors need access to reliable and comparable data.

An Accounting Model to Measure Progress Towards Living Wages

Until now, there has not been a generally agreed, straightforward and measurable way for companies to reflect their work to achieve living wages in their public reporting. As a result, investors, civil society and other interested stakeholders have not been able to access the information they need to compare companies’ progress, assess which are contributing to the solution and push those sitting on the sidelines to play their part.

“To get more companies to walk the talk on paying a living wage, we need to define what success looks like, and how to measure progress along the way. And we need common metrics for companies to account for that change in their public reports. Only then can markets reward those companies that are part of the solution to today’s growing inequalities, and push others to play their part.”

Caroline Rees President of Shift

The Accounting for a Living Wage project has resulted in a model that helps paint a picture of the scale and scope of the living wage deficits experienced by workers, as well as progress towards living wages over time. Having a shared and simple methodology to track and report on progress has proven key to the success of similar efforts to embed sustainability goals in business decision-making. This Living Wage Accounting Model has the potential to play a catalytic role in:

Delivering greater transparency regarding the payment of Living Wages

Informing new standards around Living Wages

Creating incentives for improving wages and reducing inequalities.

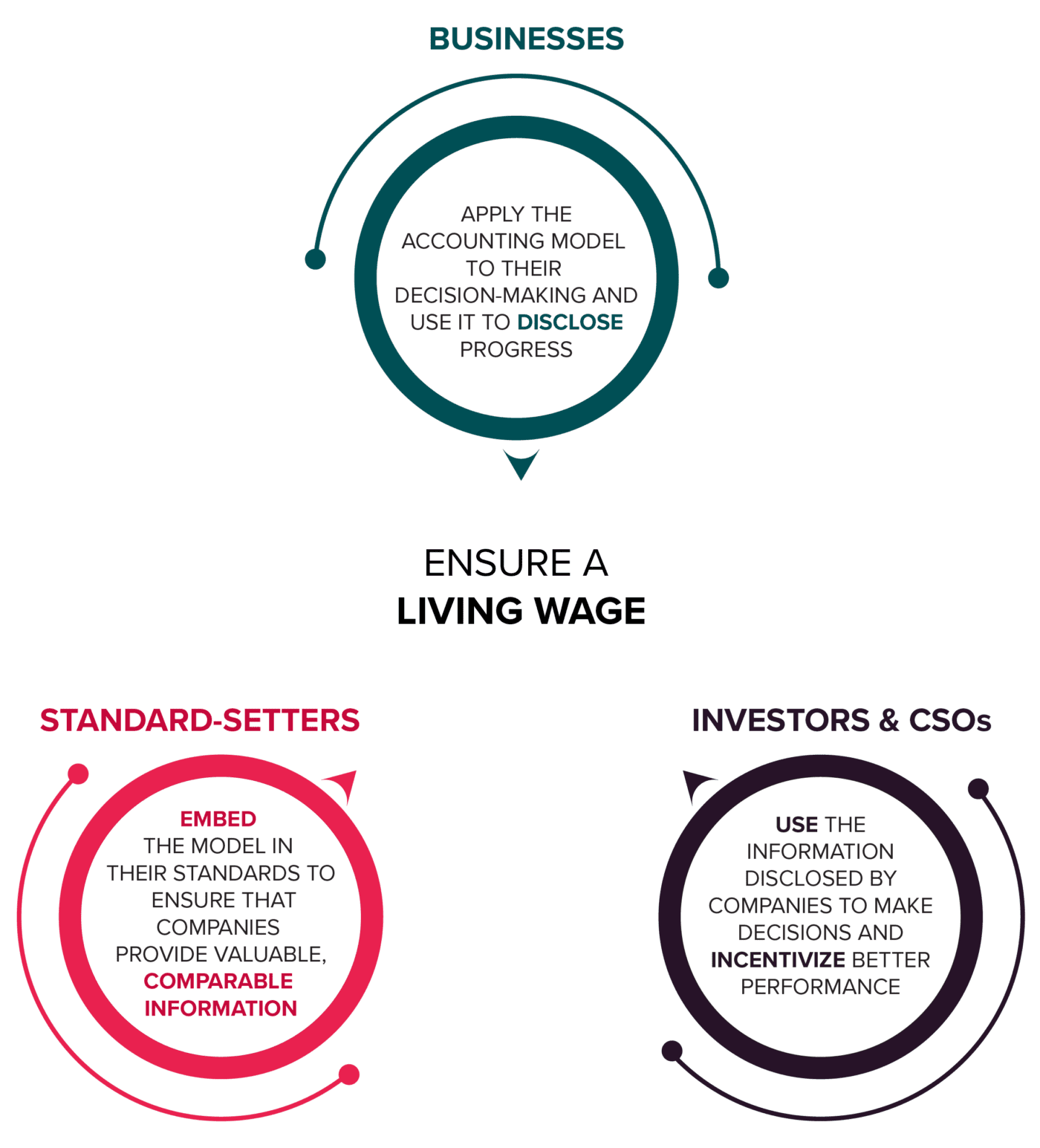

These resources are designed to support the work of:

Businesses – who can use the model and tool to measure and disclose their progress on living wages in a standardized way

Standard setters – who can embed the model in their standards to ensure that companies provide valuable, comparable information

Investors and CSOs – who can use the information disclosed by companies to make assessments and incentivize better performance

The Living Wage Accounting Model Tools

3 resources

September 2023

A Model to Measure Progress on Living Wages

The background to the project and the rationale for developing a model to measure progress on living wages.

The metrics, basic and expanded disclosures and accompanying statements of methodology that companies can follow to measure and report their progress on living wages.

A set of additional disclosures that draw on existing indicators related to living wages. When used in conjunction with the Accounting Model, these disclosures provide companies with a comprehensive Living Wage Reporting Framework that follows the ISSB four-part framework of Governance, Strategy, Risk Management and Targets and Metrics.

Coming Soon:Living Wage Progress Tool A customizable and downloadable tool that facilitates use of the model by performing all the calculations needed for the disclosures, based on wage and related data entered by companies.

The world’s current economic model – one that prioritizes short-term financial returns for shareholders over shared prosperity and decent pay, is unsustainable. Inequality is growing across the planet, and it has become one of the most pressing systems-level risks that societies face, alongside the climate emergency. A structural solution of the magnitude that is required demands that businesses, investors, standard-setters and civil society take action.

Companies – and their stakeholders – are starting to recognize the power that ensuring a living wage

( A living wage is the minimum income necessary for a worker to meet the basic needs of themself and their family, including some discretionary income. This should be earned during legal working hour limits (i.e. without overtime). The right to earn a living wage is enshrined in article 23 of the Universal Declaration of Human Rights. )

, in their own operations and across their supply chain, can play in this urgent transformation. It is also part of the responsibility that all businesses have to respect human rights in line with the UN Guiding Principles on Business and Human Rights. The good news is that more and more companies are recognizing the importance of paying living wages and making commitments and progress in that direction. The bad news is that there is a long way to go before this becomes the norm for all companies.

That’s at least partly because:

Current accounting rules view wages as a cost on the balance sheet; failing to recognize the social and human capital value of people to the business.

There is no generally agreed, straightforward and measureable way for companies to account for their work to ensure a living wage in their public reporting.

Standard setters have therefore been constrained to looking at whether companies have made commitments to living wages, without a basis for seeking more rigorous information on the results achieved.

As a result, investors, civil society and other interested stakeholders lack the information needed to compare companies‘ progress, assess which are contributing to the solution and push those sitting on the sidelines to play their part.

A shared and simple methodology to track and report on progress has been a key element of success in similar efforts to embed sustainability goals in business decision-making, for example, to reduce greenhouse gas emissions and close the gender pay gap.

An Accounting Model to Report on Progress Towards Living Wages

Shift and the Capitals Coalition have joined forces to develop an accounting model that companies can use to measure and report publicly on progress towards living wages across their workforces and supply chains over time. We aim to design a model that helps both businesses and standard-setters. For companies, it must help show the value both to society and to the business of living wages. For regulators, it must be capable of integration into accounting and reporting standards, as part of the developments in sustainability disclosures.

WE ARE DEVELOPING AN ACCOUNTING MODEL THAT CAN HELP:

The accounting model aims to:

Enable standardized disclosures in a company’s annual report, much like those for greenhouse gas emissions or the gender pay gap.

Apply not only to a company’s employees, but to its wider workforce (including those in forms of contingent labor) and workers in at least its first-tier supply chain.

Look not just at the status of workers in relation to a living wage at a point in time, but measure progress over time towards living wages for workers who are yet to reach that threshold.

WHY AN ACCOUNTING MODEL?

An accounting model through which companies can publicly disclose the value of living wages can play a catalytic role in delivering greater transparency, informing new standards and creating incentives for improving wages and reducing inequalities. This is essential to rebuild economies that advance human dignity and equality – our social and human capital – across the world.

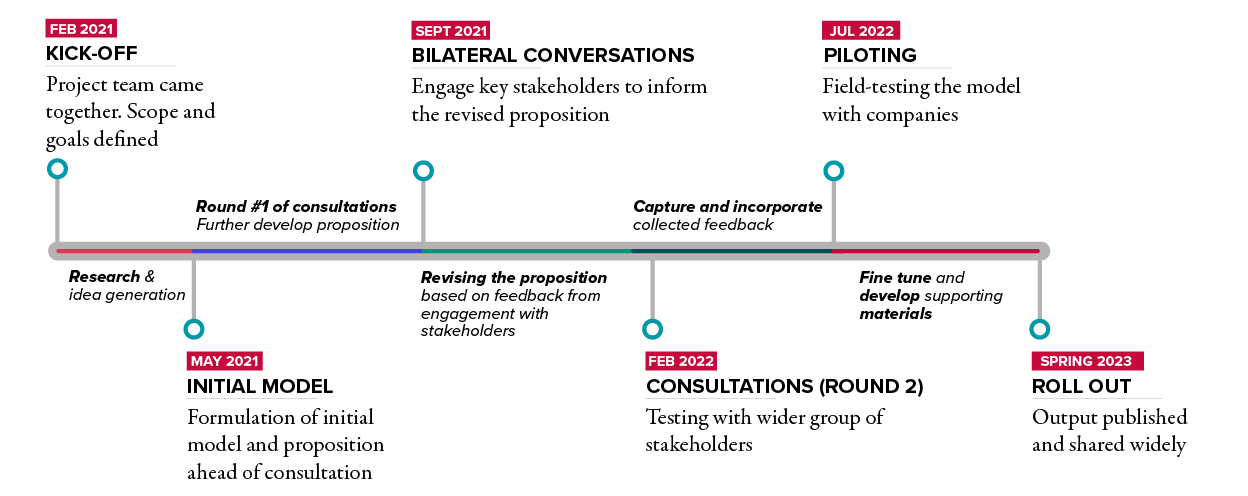

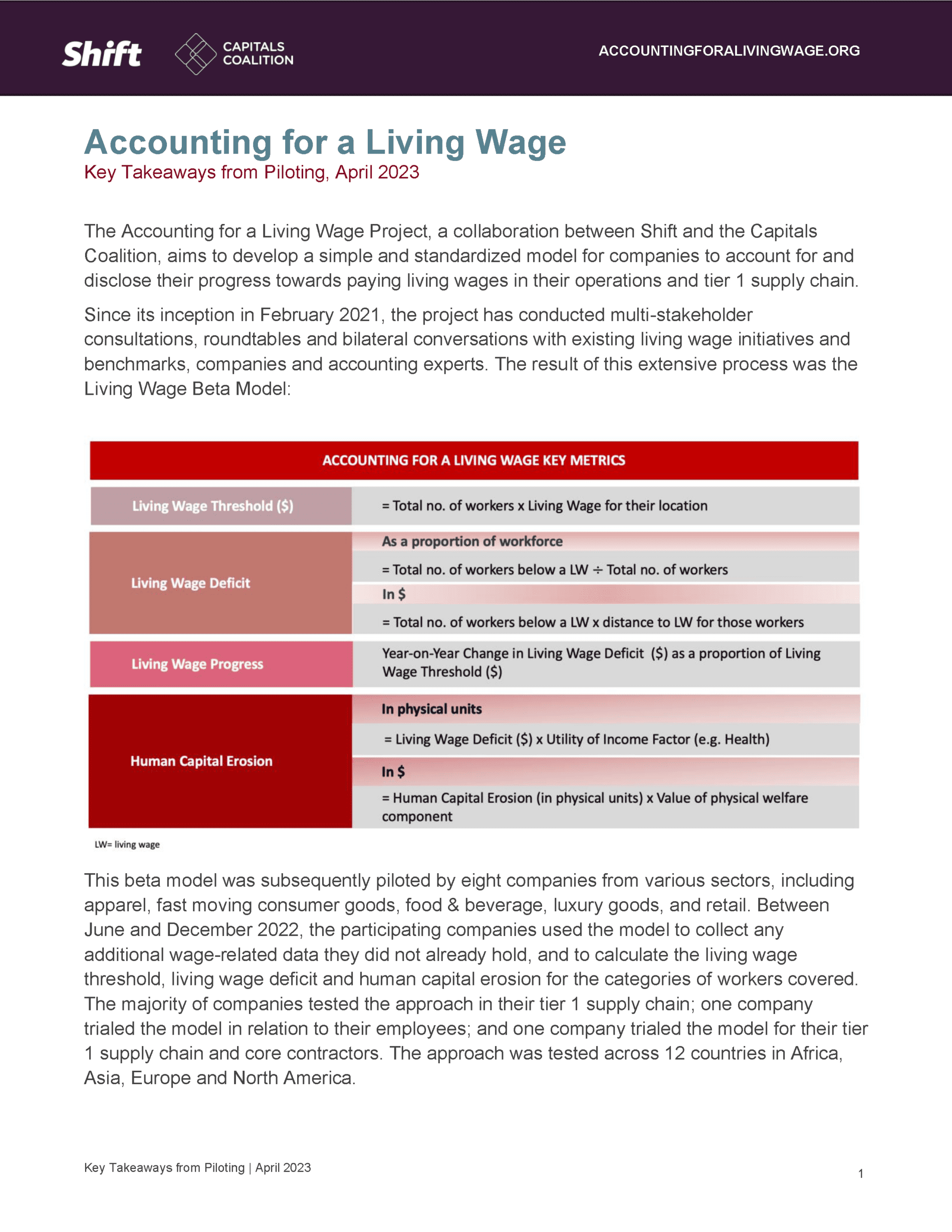

After extensive conversations and consultations with representatives of living wage benchmark methodologies and initiatives, accounting experts, companies and investors (see summaries), Shift and the Capitals Coalition have arrived at a Beta version of the Living Wages Accounting Model, that is now being piloted with companies.

The Beta model metrics are organized under three disclosures:

The Living Wage Threshold

The Living Wage Deficit

Human Capital Erosion

These unique core metrics are accompanied by a broader set of proposed disclosures, which are organized according to the four-part framework set forth by the Task Force on Climate-Related Financial Disclosures (TCFD) and adopted by the International Sustainability Standards Board (ISSB), based on ‘governance’, ‘strategy’ and ‘risk management’ in relation to living wages, in addition to ‘targets and metrics’. This model is now being piloted by a select group of small and large companies, to assess the viability of the model and the value of the insights it brings. The pilots began in July 2022 and will finish in December. A final version of the model, along with accompanying resources, will be published in spring 2023.

“People are at the core of business, yet vital information about how to nurture this ‘stock’ of human capital is omitted from today’s accounting rules. This model will help companies to actively understand and prioritize where their impacts and dependencies on people lie; where they create or erode value for communities due to their wage practices and how to disclose the progress the are making towards addressing this by paying a living wage.”

SUMMARY OF PILOTING: KEY TAKEAWAYS FROM PILOTING BETA MODEL WITH COMPANIES

Between June and December 2022, the project piloted the Beta Model with 12 companies. This takeaway document summarizes learnings and discussions from the piloting process and from a webinar held on 9 February 2023.

Interim Discussion Paper – Accounting for a Living Wage

This is an interim paper that was circulated among participants of multi-stakeholder consultations held in February 2022 to serve as a basis for discussion. It is intended as a working proposition, which is being further refined and tested by piloting companies. It does not represent the final output of the project.

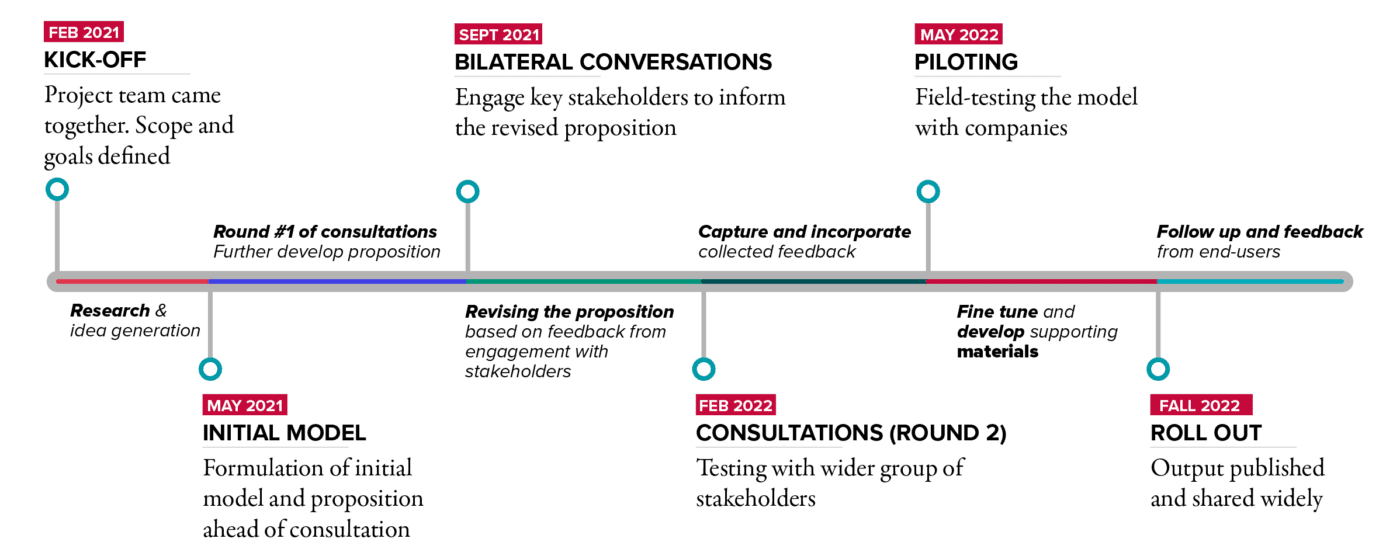

In February 2022, Shift and the Capitals Coalition held two multi-stakeholders consultations bringing together representatives from companies, leading living wage initiatives, and accounting experts to refine the proposition of the accounting model. Building on the earlier discussions and extensive bilateral conversations, the consultations focused on workable disclosures to report progress towards paying living wages. The take-aways document summarizes the key points of discussion and reflections.

Shift and the Capitals Coalition held two consultations with companies and leading initiatives in the field of living wages to discuss early stage propositions for key inputs to the proposed accounting model, most particularly: how to categorize the workers covered by the model; how to measure actual wages for workers in all categories; how to select a living wage benchmark as a basis for identifying the workers for whom wage progress is most needed. The take-aways document summarizes the key points of discussion and reflections.

One of three consultations with key stakeholders, Shift and the Capitals Coalition met with accounting experts and economists to discuss early stage propositions regarding key inputs to the proposed accounting model. This consultation focused on the potential accounting model to which data on actual wages and living wage benchmarks would be key inputs. The take-aways document summarizes the key points of discussion and reflections.

The ‘Accounting for a Living Wage’ initiative is a partnership between Shift and the Capitals Coalition. The core project team involves a number of experts in living wage methodologies and initiatives, accounting and financial modelling, human rights, human and social capital, business practices and supply chains, and economics:

An iterative process of research, consultation and gradual crystallization

The ‘Accounting for a Living Wage’ project is based on an iterative process of research, consultation with a wide array of stakeholders and other experts, and the gradual crystallization of ideas as we move towards the contours and content of a potential accounting model.

As part of our consultations, we are engaging directly with companies that are working on living wage issues. Our aim is to work with a few that are ready to test the approach we come up with. Through these pilots, we will fine-tune versions of the model to check its practicability, results and benefits.

A living wage is the minimum income necessary for a worker to meet the basic needs of themself and their family, including some discretionary income. This should be earned during legal working hour limits (i.e. without overtime).

The Universal Declaration of Human Rights makes clear that, “Everyone who works has the right to just and favorable remuneration ensuring for himself and his family an existence worthy of human dignity.”

Living wages can in turn contribute to the fulfillment of the human rights to food, water, health, adequate housing, education, family life, fair working hours and so forth.

Providing living wages can therefore contribute to the achievement of an array of Sustainable Development Goals, such as Ending Poverty, Ending Hunger, Ensuring Healthy Lives, Reducing Inequality, Decent Work, Gender Equality and others. (See this resource).

Why is it important to ensure a living wage?

Implementing a living wage is a powerful tool in reducing inequality and its negative impacts across capitals.

Our current economic model is underpinned by practices that prioritize short-term financial returns for shareholders over sustainable prosperity within planetary boundaries that benefits all stakeholders. Coupled with the perception of wages as costs rather than investments, these practices directly contribute to growing inequality around the world with negative knock-on impacts on human and social capital and, in turn, on businesses, too.

During COVID-19 we have seen both the disproportionate impacts suffered by low paid workers, and the dependency of businesses and society on their work and well-being.

The value of this business dependency is currently missing from company and investor decision making. Accounting for the value of a living wage will change that.

How does this project relate to other living wage initiatives?

Our focus is on developing an accounting model that can be used by companies not only for internal management purposes but also in public reporting to express in simple and comparable terms the progress toward living wages in their operation and supply chains.

We have been learning from a range of living wage initiatives, including those developing or assessing living wage methodologies and benchmarks, and those collaborating with companies in different sectors on practical ways to advance towards living wages.

We are also liaising with other initiatives that take an accounting lens to the question of living wages, notably Harvard Business School’s Impact Weighted Accounting Initiative, and the OECD’s Business for Inclusive Growth (B4IG) initiative on living wages. While each takes a distinct approach to our own project, we will focus on shared learning, complementarity and added value, distinguishing between value to workers, value to companies and value to society.

Will you develop a methodology to measure what living wages should be across different geographies?

No. Rather, we look to learn from those who have developed respected methodologies and how we might use them as an input to the accounting model.

I want to help. How can I get in touch?

We are always pursuing opportunities to expand and test our thinking. If you are an expert, have done research related to this topic, are a stakeholder who is interested in taking part, or know of inputs that may be valuable to our work, please contact us.

Get notified whenever Shift releases a new resource, viewpoint, or insight.

This website uses cookies to improve your experience. We'll assume you're OK with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.