Many financial institutions (FIs) struggle to define what good social performance looks like in practice.

Building on our recent work with banks, insurers and investors, Shift has published a report on Social Performance Measurement: Practical Insights and Tips for Financial Institutions. The paper sets out what works — and what doesn’t — when building insightful, decision-useful approaches to measurement.

We offer eight practical tips for moving beyond measuring basic inputs and activities (e.g., “number of human rights assessments completed”, “number of trainings delivered”) toward indicators that capture changes in business practice and behavior, as well as outcomes for people. These tips are organised around the three dimensions that FIs need to measure:

their own efforts to embed human rights due diligence

the performance of clients and investees; and

progress on specific high-priority human rights issues (such as living wage or land rights)

Along the way, it addresses key challenges and misperceptions that can often hold this work back.

The resource is written for practitioners inside financial institutions – sustainability and human rights leads, due diligence program owners, risk officers, and investment and credit professionals – looking to build, refine, or defend a credible measurement approach in an environment where demonstrating ‘what good looks like’ is of increasingly value and importance.

It will be equally useful to those who hold financial institutions to account on their human rights performance – civil society organizations, benchmark managers, regulators, auditors and asset owners – by reinforcing a shared language and a sharper set of questions for engaging the institutions they monitor.

If you are keen to take stock of where your approach sits today, and to better understand where it could go next, we invite you to take a closer look.

Today’s financial institutions (FIs) are operating in a global geopolitical context marked by multiplying conflicts, shifting political alignments and a decline in respect for international law. Moreover, technological developments are redefining the methods of conflict.

In this environment, FIs face growing pressure from governments to navigate defense-related clients and transactions in ways that support evolving security priorities. They also have strong commercial incentives to participate in a rapidly expanding sector.

At the same time, institutions remain bound by longstanding commitments to responsible investment and lending practices. And we continue to see a large body of data showing that conflict -including the impacts on people’s human rights arising from conflict -creates business and investment risks for financial institutions.

Importantly, in a turbulent geopolitical context, institutions that adapt their policies and decisions in response to one particular conflict can quickly find themselves applying those policies to very different conflict situations, where alliances, actors and the justifications for the use of force are far less settled.

Against this dynamic backdrop, financial institutions face a practical question: how should human rights due diligence be approached in relation to companies developing, producing, brokering, selling or exporting weapons and dual-use technologies?

Shift has worked for many years with investors and lenders to help them understand and address human rights risks across their portfolios, with a growing focus on conflict-affected and high-risk contexts, particularly since the war in Ukraine. Through this work, we have observed recurring challenges in navigating complex, incentive-laden decisions, and while there are no simple solutions, there are stable anchors that can guide institutions through this rapidly evolving terrain.

This paper

sets out particular challenges faced by practitioners within financial institutions who are tasked with managing human rights risks when it comes to defense-related lending and investing;

sets out some key ‘anchors’ in international humanitarian law that set important parameters on decision-making by financial institutions; and

discusses additional approaches that financial institutions can take as part of their human rights due diligence to strengthen their decision-making and better manage risk to their clients and to their own institutions.

Action to address climate change is urgent and essential for our shared future. This action should shape better lives for all, not leave the poorest and most marginalized left out and worse off.

We already see the consequences of today’s high levels of inequality all around us in social polarization, political backlash, economic protectionism and instability. Climate action that fuels these dynamics will only increase opposition to the kinds of changes we need to build a more sustainable future.

Instead, we need to achieve what is termed a ‘just transition’ – a transition to a low carbon and climate-resilient future that prevents or minimizes harm to vulnerable workers, communities and consumers.

Companies, standard setters and financial institutions increasingly recognize the need to bring a human rights perspective to climate action in service of a just transition. And standard-setters are already reflecting these expectations in the laws, regulations and other standards they develop.

We see more and more organizations using narrative – or ‘qualitative’ – indicators to describe how human rights considerations are integrated into companies’ efforts to mitigate and adapt to climate change. But we are also hearing an increasing number of organizations call for quantitative, measurable data, to complement these qualitative indicators, to provide a more comprehensive and tangible picture of how impacts on people from climate action are being managed.

As a result, it is clear that quantitative metrics are also needed to measure what is working and what isn’t, to know which are the successful approaches that should be scaled and replicated, and to be able to account for the results.

Shift has been working with a number of other organizations doing leading work in support of a just transition, to build broad consensus around a core set of quantitative, sector-agnostic metrics. These Just Transition metrics can supplement qualitative indicators and help provide the full picture necessary to assess the ‘justness’ of the climate transition.

This set of metrics does not – because it cannot – address all scenarios and variations. However, we believe they provide a sound foundation upon which additional metrics relevant to specific sectors and geographical contexts can be layered.

Throughout the development of the metrics, Shift and our collaborating partners have intentionally kept them within the realm of data that can reasonably be gathered and provided by companies, while recognizing – and hoping – that the art of the possible will improve over time.

The intent is that these metrics can be applied in the context of full ‘transition plans’ or in relation to more diffuse activities targeted at the transition. In either case, the metrics would apply within the same ‘boundaries’ – in terms of facilities, locations or other fields of action – as those plans and activities and their associated climate metrics.

The final set of just transition metrics should be one that can be embedded in sustainability reporting standards alongside important contextual information. Figure 1 illustrates how they might fit into the four-pillar structure that is common to many reporting standards today.

Figure 1

GOVERNANCE

– High-level oversight of policy/strategy/transition planning – Human Rights Due Diligence process linked to transition planning and implementation – Approval of targets

STRATEGY

– Commitments to Just Transition, decent jobs, social dialogue – Identification of, and meaningful engagement with, affected stakeholders – Workforce composition

RISK AND IMPACT MANAGEMENT

– Highest risk and impact climate actions and locations -Measures taken to mitigate risksand impacts – Process for identifying and addressing skills gaps and opportunities

METRICS & TARGETS

– Job security – Reskilling, upskilling and redeployment – Remuneration & living wage – Engagement with workers and communities

This version of the metrics builds on our experience working with the Global Reporting Initiative, which has made ground-breaking progress as part of GRI 102: Climate Change Standard, as well as an earlier set of metrics we published in April 2025. This most recent version reflects collaboration and consensus across a range of organizations around the current “best-in-class” metrics.

It is our hope that these metrics bring clarity and value to all stakeholders: companies themselves as they try to measure what matters; data providers and investors who need this information for their own services and decisions; and reporting standard-setters needing to ensure consistency for preparers and insight for users of disclosed information.

We will continue conversations with interested organizations in the months ahead, including to learn more about the use of these metrics in practice, and how they can be further improved and added to in light of experience and further data availability. We welcome all inputs and advice as part of this continuing exploration.

Click here to download an Excel spreadsheet containing our Just Transition Metrics.

This page will host a forthcoming report, to be published in May 2026, on the financial effects of engagement with Indigenous Peoples and local communities in relation to nature-related impacts. Please check back soon.

About the EU Corporate Sustainability Due Diligence Directive

Beginning in 2017, several European states including France, Germany and the Netherlands began to adopt versions of mandatory human rights due diligence legislation. This created momentum for the European Union (EU) to help level the playing field, recognising that voluntary corporate action alone is not sufficient to drive change in how people are treated in global value chains at the scale and pace that is needed.

In 2022, the EU began negotiating a draft Corporate Sustainability Due Diligence Directive (CSDDD) which was finally adopted in May 2024. Throughout the two years of negotiations, Shift was focused on engaging with policy-makers in EU Member States and in the European Parliament to help ensure the CSDDD was anchored in the international standards on sustainability due diligence – the UN Guiding Principles on Business and Human Rights and the OECD Guidelines for Multinational Enterprises. Many other stakeholders also supported this call, including thousands of companies. Despite limitations with regard to the scope of companies covered under the Directive, and limited obligations with regard to due diligence on downstream business relationships, the core content of the final law was substantially aligned with the UNGPs.

Shortly after the CSDDD was enacted, the President of the European Commission announced that the Commission would bring forward a proposal to simplify requirements and reduce burdens on European companies, including in relation to the CSDDD (which had not yet even entered into force for covered companies) and the more established Corporate Sustainability Reporting Directive (CSRD). In February 2025, the Commission announced its ‘Omnibus Simplification Package I’ (‘Omnibus’). While the goals of the Omnibus were broadly reasonable ones for EU policy-makers to pursue, in fact the proposal would have made life more complicated for covered companies by requiring them to carry out parallel due diligence processes without providing meaningful protections for smaller business partners – as we explained in our March 2025 assessment of the Omnibus Proposal.

Alongside individual companies and business associations that support the UNGPs, and our civil society allies, Shift was actively involved throughout the Omnibus process to push for continued alignment with the international due diligence standards.

Where did the final CSDDD land?

In December 2025, a political agreement was reached that preserved the core of the risk-based due diligence approach in the CSDDD, as we explained in our assessment of the result. The revisions to the CSDDD were confirmed by the European Parliament and by Member States in the Council of the EU in February 2026.

The final CSDDD sets a mandatory regional standard that will have an impact not only in Europe but well beyond. Although the scope of companies covered by the Directive following the Omnibus process was reduced to only the very largest companies operating in the EU, the impact of the legislation will extend significantly beyond those companies and into their global value chains.

Crucially, the due diligence duty in the CSDDD remains substantially aligned with the international due diligence standards, making it more likely to be impactful in practice for workers and communities while remaining feasible for companies to implement. The CSDDD thus helps level the playing field for companies that have been implementing the international standards for 15 years.

EU Member States now have to transpose the CSDDD into their national laws by mid-2028 and enforcement will start from mid-2029. Meanwhile the European Commission is mandated to develop authoritative guidance on the due diligence duty that will influence enforcement by national regulators and through civil litigation.

Throughout the uncertainties created by the Omnibus process, and now as EU Member States prepare to implement the CSDDD, our advice to companies that want to know how they should respond remains the same – keep doing risk-based due diligence in line with the UNGPs. That remains the single best investment companies can make to prepare to meet current and future legislative and wider demands, whether from investors, lenders, customers, civil society or EU policy-makers. That is particularly true as other jurisdictions – including Switzerland, the UK, Australia, Thailand and Indonesia – now move to advance or debate proposals on mandatory human rights due diligence grounded in the UNGPs.

Core Resources

Our analysis

4 resources

December 2025

Shift statement on the political agreement on the Omnibus Simplification Package on EU sustainability due diligence and reporting rules

December 10, 2025 _____ On Monday, 8 December, EU Member States and the European Parliament reached a provisional political agreement in trilogue negotiations – together with the European Commission – on the Omnibus I process to revise both the Corporate Sustainability Due Diligence Directive (CSDDD) and the Corporate Sustainability Reporting Directive (CSRD). The rushed and […]

The European Commission’s ‘Omnibus Simplification Proposal’: Shift’s initial reflections

06 March 2025 The European Commission has launched its Omnibus Simplification Proposal to address concerns about sustainability regulations in the EU. But measured by its own objectives of simplifying requirements and reducing burdens on smaller companies, the proposals are a remarkable own goal. Negotiations in the coming months must be grounded in a practical grasp […]

Designing an EU Due Diligence Duty that Delivers Better Outcomes

What is the CS3D? Starting in 2022, the European Union has been negotiating a draft Directive on Corporate Sustainability Due Diligence (CS3D), with discussions on a final law expected to begin by mid-2023. The draft Directive aims to ensure companies active in the single European market contribute to sustainable development by preventing and addressing negative human rights and environmental impacts. […]

Aligning the EU Due Diligence Directive with the International Standards: Key Issues in the Negotiations

Aligning the CS3D with the core concepts in the international standards The EU is currently in the process of negotiating a legal instrument that will establish new corporate human rights and environmental due diligence duties across the single market – the draft Corporate Sustainability Due Diligence Directive (CS3D). At the heart of the negotiations is […]

Our March 2022 ANALYSIS of the Commission’s proposal for a draft Directive

Our October 2021 Key Design Considerations for the Enforcement of Mandatory Due Diligence, developed in collaboration with the Office of the UN High Commissioner for Human Rights

This series captures the research findings from our analysis of 3073 social and governance indicators used in ESG data providers’ products or reporting requirements.[1] In our Guardrails, we focus first on the problems, spotlighting the types of indicators that offer minimal insight, or worse, incentivize poor practices. In our Guidelines, we then turn to indicators and metrics that are more robust, illuminating the pathway to better measurement. In our Thematic Deep Dives, we review ESG indicators related to specific issues (Occupational Health and Safety, Living Wage, Community-Focused Impacts). These deep dives identify pitfalls in indicator formulation as well as good practices that can inform better measurement of companies’ social performance on these topics.

Across the series, we will exemplify the good, bad and ugly of social indicators and metrics. Our goal is not to offer yet another set of competing indicators, but to share what we’ve learned about good indicator design in order to inform healthy debate, collaboration and innovation to improve the S in ESG.

This series is for everyone and anyone working to improve the ways in which we evaluate companies’ social performance.

Deep Dive Series

A series of deep dives evaluating better social indicators and metrics for occupational health and safety, living wage, and community-focused impacts.

3 resources

DEEP DIVE 01: Occupational Health and Safety Indicators

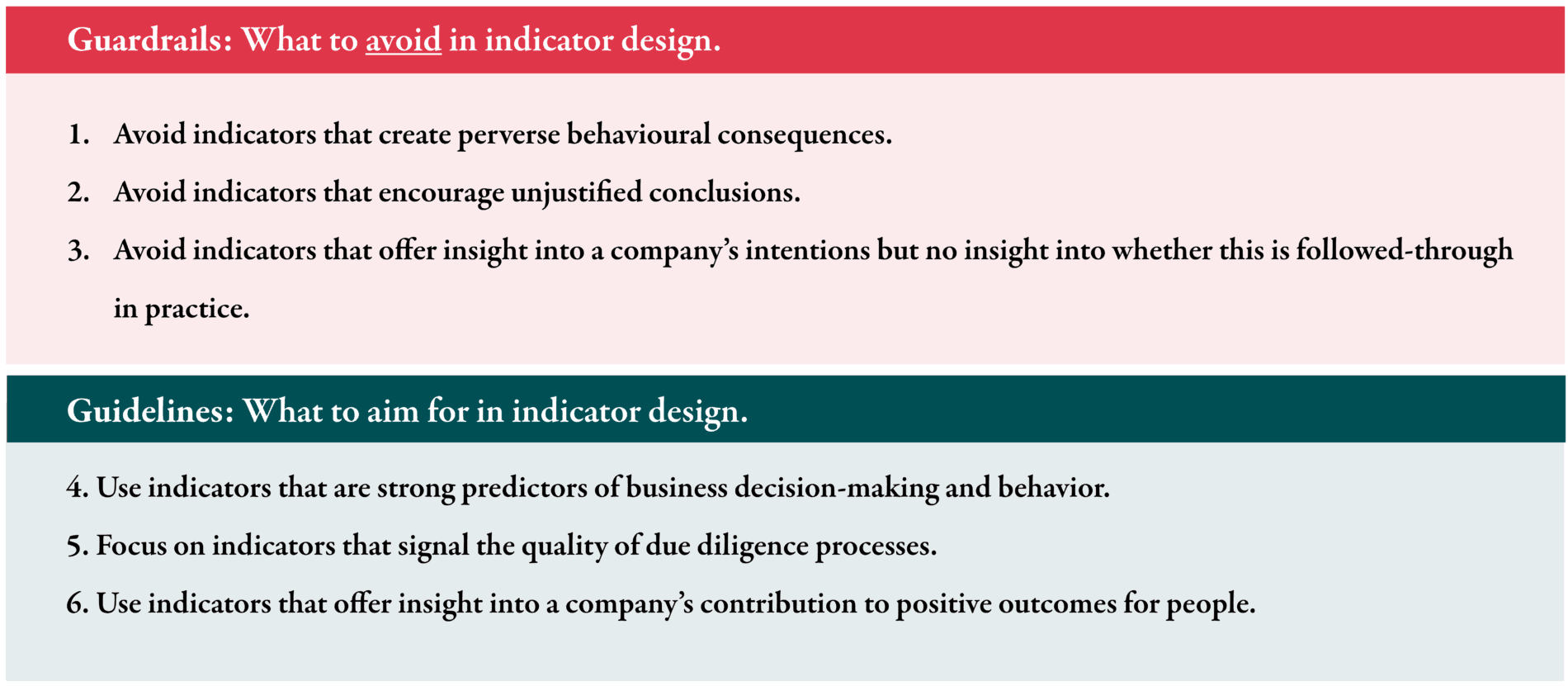

In climbing, guidelines are cords or ropes to aid passers over a difficult point or to permit retracing a course. Guardrails are physical barriers used to prevent people from falling from a height or from straying from a pathway or road into dangerous areas. So, both are put in place when the journey and terrain may be hard to navigate.

In the context of designing social indicators and metrics, we need both guardrails and guidelines, so we’ve structured our initial findings within the series around these.

If we fail to reclaim the measurement of companies’ social performance as a tool to advance business respect for human rights, the S in ESG will remain divorced from the investor and business decisions that determine whether business is done with respect for people’s dignity. We hope this series can play a part in sustaining, advancing and scaling practices that lead to better outcomes for workers, communities and the people impacted by the use of products and services.

Guardrails

A series of guardrails for designing better social indicators and metrics.

3 resources

May 2024

Guardrail 01: Avoid indicators that create perverse behavioral consequences.

The field of sustainability and responsible business conduct is faced with a significant opportunity: to coalesce around a core set of select, standardized indicators and metrics that meaningfully measure companies’ social performance regardless of their industry sector. This is key to equipping investors, business leaders, regulators and civil society with the tools to push to scale business practices that are in line with the principle of basic dignity and equality for all.

Success will significantly contribute to tackling inequalities, ensuring business actions towards net zero and net positive have the social license to proceed at the urgent pace required, and adapting business models and global value chains so that they deliver resilience to businesses and the stakeholders they impact. Failure risks ushering in more, already well-catalogued business-related harms and risks to people, planet and prosperity, likely with evermore multi-generational consequences.

The good news is that most stakeholders have embraced the pressing need for convergence around corporate sustainability reporting standards, including the indicators and metrics against which companies should disclose information and that should be used to evaluate corporate performance. Even better, recent institutional coordination and collaboration has set the stage for well-governed and inclusive processes needed to achieve such convergence.

Barriers to strengthening the S in ESG

Any ambitious project has risks that need managing. The challenge of building consensus across diverse stakeholders around indicators and metrics that offer credible insight into a company’s social performance is no exception.

Some risks are the consequence of positive dynamics. For example, the welcome growing attention to the S in ESG has resulted in thousands of social indicators and metrics already being developed by mainstream data providers and more targeted ranking and rankings. But the risks is that in a bid to identify a smaller set of indicators, we select the most commonly used indicators, in spite of broad recognition that these may not be fit for purpose.

In addition, the urgent need to effect a step change in the scale and quality of corporate reporting and assessment on social issues also carries the risk that project timelines prevent us from interrogating the devil in the detail of indicator formulations, such as when indicators may have perverse, unintended consequences.

The consequence of such risks is more than inconvenience and frustration. We could end up with solutions that confuse decision-makers, reflect the lowest common denominator of thinking and practice, or fail to ward off critiques of blue-washing and corporate capture, but also of so-called woke capitalism.

[1] Shift was unable to verify whether the non-public indicators and metrics that we used for our analysis are the most up to date versions used by data providers at the time of writing (April 2024). We also recognize that the underlying methodologies used to reach a judgement on a company’s performance against an indicator may offer more nuance that we could not access for our research.

Shift’s Business Model Red Flags is a set of indicators that may be found in dominant or emerging business models in and across a range of sectors. They are not intended to be an exhaustive list but may help spark reflection and enable the identification of additional red flags.

In September 2025, 13 of the 25 Red Flags were updated and expanded to integrate a climate lens. The revised tool now features 14 climate-linked Red Flags — 13 updated and one newly developed — each illustrated with real-world examples of corporate action and material consequences that have arisen where a business has failed to mitigate the risks inherent in its business model.

THE BUSINESS MODEL RED FLAGS ARE INTENDED FOR THE USE OF

Business leaders seeking to identify and address risks to people that may be embedded in the business model, in order to ensure the resilience of value propositions and strategic decisions and build more integrated approaches to climate and human rights risks and impacts.

Lenders and Investors scrutinizing their portfolios for human rights risk, including as it pertains to climate action, engaging with clients and investees and diagnosing whether significant human rights incidents are likely to be repeated by the company concerned, replicated in other parts of their portfolio or are being hard-wired into company climate strategies and transition plans.

Regulators, analysts and civil society organizations seeking to strengthen their analysis and engagement with companies and investors on business model-related risks to people, including how they may be interacting with climate-related risks.

There are 25 Business Model Red Flags

(To see an overview chart with all 25 red flags, click here)

The Red Flags are organized around three features of a business model:

HOW EACH RED FLAG IS ORGANIZED

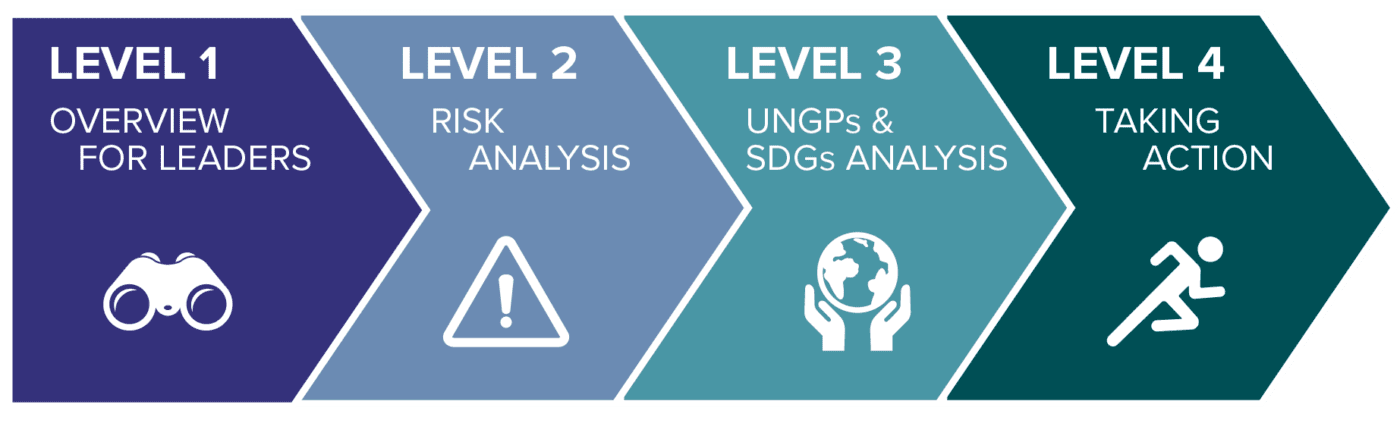

Each red flag is supported by a guidance document, organized into four levels:

Level One: Overview for Leaders

This includes:

Higher risk sectors in which the red flag feature is most prevalent;

Key questionsfor leaders to ask or be asked to aid decisions about whether further action is needed.

Level Two: Risk Analysis

This includes:

Risks to People: the key human rights risks associated with this red flag, absent appropriate mitigation efforts;

Risks to the business: evidence of legal, financial, operational and reputational risks that can arise as a result of companies not addressing the red flag.

Level Three: UNGPs and SDGs analysis

This sets out:

What the UNGPs say, with particular reference to how companies might be involved with the adverse human rights impacts associated with the red flag;

Possible contributions to the Sustainable Development Goals that can be achieved with effective mitigation or removal of the red flag;

Level Four: Resources for taking action

This includes:

Due diligence lines of inquiry for deeper analysis of the company’s impact and how it could effectively mitigate the risks associated with the red flag;

Mitigation examples illustrating how companies have in practice sought to reduce the impacts associated with the red flag;

Alternative model examples of companies that have either designed or redesigned their business model to function without the risk elements highlighted in the red flag;

Additional tools and resources to guide further analysis.

Examples of Investor Application of Red Flags

Institution

DD Stage Referenced

Use

Source

APG

Pension provider

Risk

Identification

Portfolio

Engagement

“Additional conditions and mitigants are required for companies operating in high-risk areas. Moreover, in partnership with the Shift Project, we are developing our model of ‘red flags’ for companies in sectors exposed to high-risk business models, such as those handling sensitive data or having complex and vulnerable supply chains. This analysis is intended to bolster our human rights due diligence efforts and improve our engagement with companies on human rights.”6

FN 6: “…Shift’s Business Model Red Flags are key indicators present in dominant or emerging business models across various sectors. While not exhaustive, they serve to prompt reflection and aid in identifying additional red flags.”

“In 2023 ABN AMRO developed a social risk identification tool (the Social Risk Heatmap), which provides a structured methodology to help us to identify human rights risks in our business environment. The Social Risk Heatmap shows potential impact in the sectors in which our clients operate. This may differ from the actual impact of our clients, which may be reduced through preventative measures taken to counter adverse human rights impacts. The risk level per sector is based on several indicators taken from the Impact Institute’s Global Impact Database and Shift’s Business Model Red Flags and focuses on four themes: labour rights, land-related rights, the right to life and health and the right to privacy and freedom of expression.”

“To set our engagement targets, we have identified key outcomes and activity indicators that focus on tangible outcomes (e.g. number of child labour incidents remediated) for land and labor rights and on effective actions to reach those outcomes (e.g. evidence of improvements on purchasing practices and of robust human rights due diligence). This approach aims to look beyond policy commitment of a company and to focus on actual results and implementation quality. Although land and labour rights are already a subset of all human rights topics, they still cover a wide spectrum of issues. Therefore, a second level of prioritization is necessary in selecting engagement targets per company. For this, we consider multiple factors, including existing controversies, social benchmarks, and business model red flags.”

Bridges Fund management Specialist sustainable and impact investment fund manager

Risk Identification Risk Assessment Mitigation through Leverage

“We assess each potential investment against the SHIFT Business Model Red Flags framework to check whether there are human rights risks inherent in the business model. Where significant risks of potential harm are identified, we carry out further due diligence to understand those risks and assess whether they are manageable. If so, we work closely with management with the aim of ensuring that the potential negative impacts are mitigated and managed.”

Wealth and superannuation platform and technology provider

Risk Identification Risk Assessment

“HUB24 takes a risk-based approach to identifying and assessing modern slavery risk in our operations and supply chain. Our modern slavery risk assessment considers the four key modern slavery risk factors of:

[1] Vulnerable populations […]

[2] High-risk geographies […]

[3] High-risk sectors […]

[4] High-risk business models: Business models that have higher human rights risks, including modern slavery risk. Examples include labour hire outsourcing with high use of precarious labour, low-cost goods and services, sourcing in countries with contested land use, and complex supply chains with limited visibility.”3Business Model Red Flags (FN3)

[Modern slavery] risks can arise due to the following factors:

[1] Sector or Categories Risk […]

[2] Country Risks […]

[3] Vulnerable Groups […]

[4] Business model risks: Business models that have higher human rights risk. Examples

-Labour hire and outsourcing with high use of precarious labour

-Franchising

-Complex supply chains with limited visibility

-Low-cost goods and services

-Sourcing in countries with contested land use.

There are 25 Business Model Red Flags. Each one is available to read online, by clicking on the word READ, or to download as a PDF. You can also use the search bar below to filter them by sector.

In September 2025, Shift updated the Red Flags to bring a climate lens to the dominant or emerging business models that are most likely to interact with climate change, and action to address it, to intensify and extend the range of human rights risks faced by workers and communities. These Red Flags are indicated by a ‘With Climate Lens’ icon.

Once you’ve picked the Red Flags you want to download, select them by clicking on the circled number of each Red Flag and choose ‘Download All Selected’. You may also choose to download the full series or to download a high level menu. For support, please contact communications [at] shiftproject [dot] org.

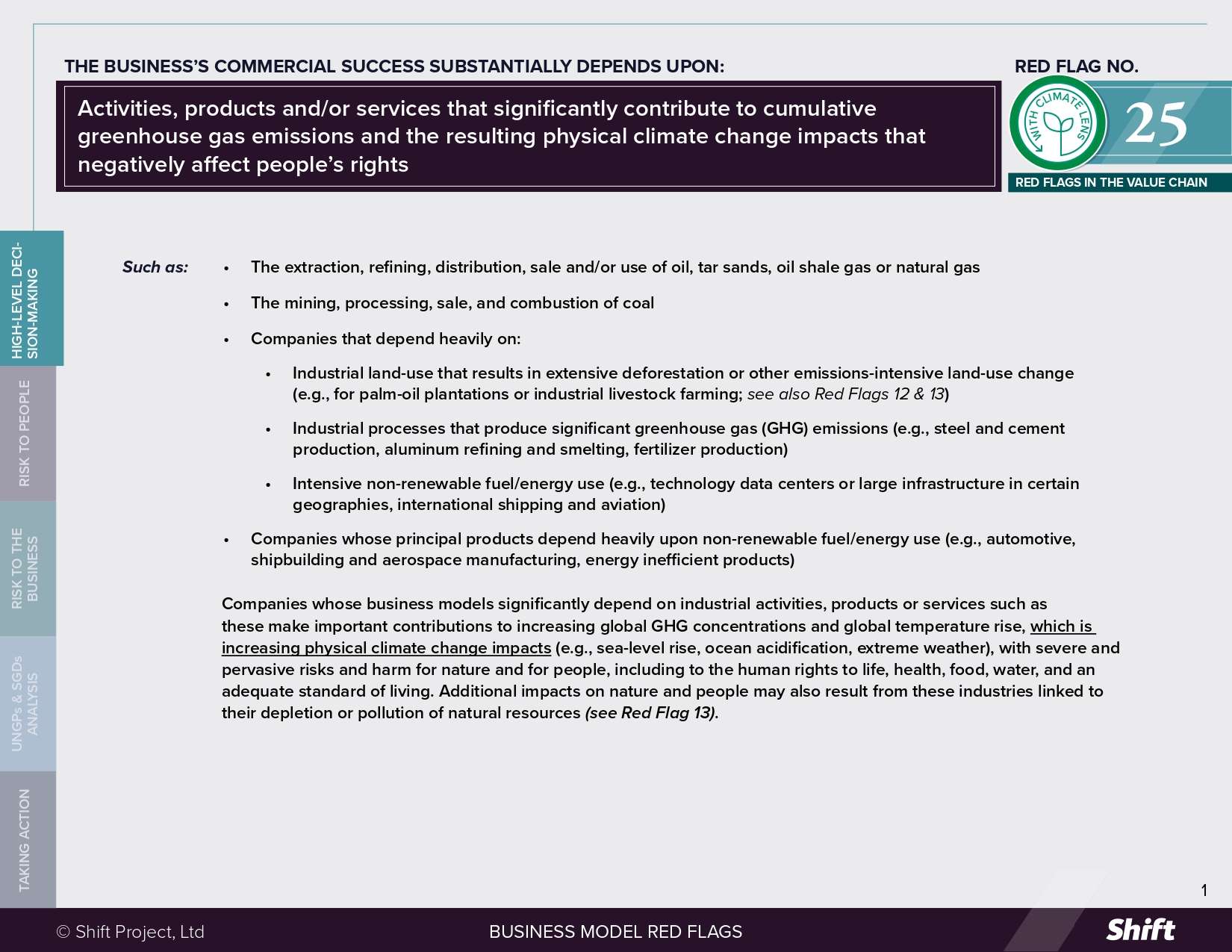

Activities, products and/or services that significantly contribute to cumulative greenhouse gas emissions and the resulting physical climate change impacts that negatively affect people’s rights

FOR EXAMPLE

The extraction, refining, distribution, sale and/or use of oil, tar sands, oil shale gas or natural gas

The mining, processing, sale, and combustion of coal

Companies that depend heavily on:

Industrial land-use that results in extensive deforestation or other emissions-intensive land-use change (e.g., for palm-oil plantations or industrial livestock farming; see also Red Flags 12 & 13)

Industrial processes that produce significant greenhouse gas (GHG) emissions (e.g., steel and cement production, aluminum refining and smelting, fertilizer production)

Intensive non-renewable fuel/energy use (e.g., technology data centers or large infrastructure in certain geographies, international shipping and aviation)

Companies whose principal products depend heavily upon non-renewable fuel/energy use (e.g., automotive, shipbuilding and aerospace manufacturing, energy inefficient products)

HIGHER-RISK SECTORS

Oil and gas exploration, extraction and transportation

Coal mining, processing and transportation

Fossil fuel-based power generation (e.g., lignite, coal, oil and natural gas)

Carbon-intensive industrial sectors (e.g., petrochemicals, steel, iron, cement, aluminum and construction inputs)

Industrial-scale conventional agriculture (e.g., industrial livestock farming, palm oil plantations, and other commercial farming activities)

Forestry and forest products

Large-scale transportation (e.g., industrial land transport, marine shipping, aviation)

Information and Communication Technology (see also Red Flag 21)

Financial institutions that are significantly financing higher-risk industries that lack robust transition planning

Companies whose business models significantly depend on industrial activities, products or services such as these make important contributions to increasing global GHG concentrations and global temperature rise, which is increasing physical climate change impacts (e.g., sea-level rise, ocean acidification, extreme weather), with severe and pervasive risks and harm for nature and for people, including to the human rights to life, health, food, water, and an adequate standard of living. Additional impacts on nature and people may also result from these industries linked to their depletion or pollution of natural resources (see Red Flag 13).

Questions for Leaders

How is your business model compatible with the objectives of the Paris Agreement?

How do you consider the impact of your climate action or inaction on people and how have you identified and engaged with potentially impacted workers (including value chain workers), communities, or consumers?

To what extent have you integrated human rights considerations into your approach to managing your climate change impacts?

Have you considered the regulatory, reputational, legal and financial risks associated with maintaining business as usual or taking insufficient action to address your climate impacts, including those risks that flow from the human consequences of your climate impacts?

To what extent have you explored potential business opportunities in developing products or services that help achieve net zero in ways that respect and advance human rights?

How to use this resource.

( Click on the “+” sign to expand each section. You can use the side menu to return to the full list of red flags, download this Red Flag as a PDF or share this resource. )

Understanding Risks and Opportunities

Risks to People

Climate change directly and indirectly affects a wide range of human rights. The UN Secretary-General has stated that “climate change is, quite simply, an existential threat for most life on the planet – including, and especially, the life of humankind”. The Intergovernmental Panel on Climate Change (IPCC), the UN Human Rights Council and the Special Rapporteur on human rights and climate change have highlighted that climate change has an impact on, among others, the rights to life, self-determination, development, health, food, water and sanitation, adequate housing and a range of cultural rights. In their landmark July 2025 advisory opinion on climate change, the InterAmerican Court of Human Rights (IACHR) recognized that climate change carries “extraordinary risks” that are felt particularly keenly by people who are already vulnerable.

Physical climate impacts will continue to increase in frequency, intensity and duration unless urgent action is taken to curb global emissions. For example, the IPCC estimates that between 2030 and 2050 climate change is expected to cause approximately 250,000 additional deaths per year, from undernutrition, malaria, diarrhea and heat stress alone.

Companies whose business models substantially rely on emissions-intensive activities, products or services play a particularly critical role with respect to the action required to address global climate change.

A 2017 report by CDP in collaboration with the Climate Accountability Institute, referring to the world’s top 100 private and public fossil fuel producers since 1988, highlighted that ‘[t]he scale of historical emissions associated with these producers is large enough to have contributed significantly to climate change. It follows that the actions of these producers over the medium-long term can, and should, play a pivotal role in the global energy transition’. In 2023, Carbon Majorsestimated of the top 20 emitters globally (states and companies), 16 are companies. According to a 2021 study by Generation Investment Management, publicly listed companies represent 40% of global GHG emissions, underscoring how much potential influence investor engagement can wield. And these emitters span sectors beyond fossil fuel producers, such as Information and Communication Technology and Aviation. Without urgent and decisive action, emissions will continue to rise.

While progress on corporate climate action is being made,the pace and scale is not commensurate to what is needed. As result, the future efforts needed will increase exponentially with each year of insufficient action. The need for transparent, credible, Paris-aligned transition plans, backed by rigorous implementation, remains acute. Such plans form the necessary foundation of a rights respecting transition to a low carbon and climate resilient economy (often referred to as a “just transition”). And yet, while many companies have set ambitious net‑zero goals, very few have published credible, detailed plans explaining how they’ll reach them. Thus, further progress in transition planning and execution is an urgent and critical imperative for tackling the corporate contribution to global climate change with all its consequences for human rights and human existence. Further, these plans must be designed and implemented in a manner that addresses potential risks and impacts to people in order to foster trust and legitimacy, as well as avoid fuelling – and reduce – the high levels of economic inequality that increase social instability, political opposition, and protectionist economic policies, all of which can ultimately undermine critical climate action.

Risk to the Business

Reputational risks: Individual company climate change impacts that affect human rights can generate considerable attention and multinational corporations are often targeted for criticism, particularly where people believe that appealing to governments may have little effect.

Even where legal action against a company relating to the human rights impacts of climate action or lack of action is unsuccessful, this can still present considerable reputational risk to the company.

In 2022, the UN Commission on Human Rights (CHR) of the Philippines published its final report finding that the world’s biggest polluting companies can be held responsible for human rights violations and threats arising from climate impacts. CHR announced that the 47 investor-owned corporations, including Shell, ExxonMobil, Chevron, BP, Repsol, Sasol, and Total, could be found legally and morally liable for human rights harms to Filipinos resulting from climate change.

In 2025, the UK charity ActionAid publicly cut ties with HSBC, citing the bank’s continued financing of fossil fuel and industrial agriculture projects—amounting to over £153 billion between 2021 and 2023—as evidence the company is consistently “choosing profit over people and planet”. Civil society groups like BankTrack, Indigenous rights advocates, and major investor coalitions such as ShareAction have raised similar concerns about HSBC’s increasing financial, legal, and reputational risks tied to climate change.

Legal, financial and regulatory risks: Companies that do not take action to address their climate change impacts can face legal action for their contribution or preemptive legal action to avoid company activities that are perceived to negatively impact local communities or other stakeholders. Since 2016, there has been significant growth in climate change-related legislation. As of July 2025, 2967 climate change cases have been filed globally. Around 20% of climate cases filed in 2024 targeted companies, or their directors and officers. According to the London School of Economics’ Grantham Institute, which analyzes climate change litigation annually, “The range of targets of corporate strategic litigation continues to expand, including new cases against professional services firms for facilitated emissions, and the agricultural sector for climate disinformation”. While highly anticipated legal decisions have faced evidentiary hurdles, they have: (a) acknowledged the connection between GHG emissions, physical climate change and impacts on people, (b) scrutinized whether companies are taking reasonable and sufficient action to mitigate their impacts, and (c) explored the principle of companies being held liable for climate-related harm. Some notable legal developments include:

Royal Dutch Shell was taken to court in 2019 in the Netherlands on human rights grounds relating to the climate impact of its business. Although Shell won an appeal of the case brought by Milieudefensie in 2024, the court emphasised that companies, especially those that have contributed to climate change, have a responsibility and power to contribute to combating climate change. Further, the court affirmed in unequivocal terms that “protection from dangerous climate change is a human right” and these rights extend to what can be required of Shell.

A Peruvian farmer filed a lawsuit against German Energy giant RWE in German courts. His case argued that because RWE’s GHG emissions—estimated at 0.5% of historical global emissions—contributed significantly to glacial melting and heightened flood risk that impacted his property in Huaraz, Peru, RWE should compensate him for 0.5% of the costs of his flood protection investments. While the case was ultimately dismissed, after multiple appeals and years of litigation, for the first time, a court affirmed that large emitters could be held civilly liable under German law for climate damage—even across borders—based on scientific attribution and proportionate responsibility.

In May 2024, Vermont became the first U.S. state to pass a “climate superfund” law aimed at holding major fossil fuel companies financially accountable for the costs of climate change. The law targets companies responsible for over one billion metric tons of GHG emissions and seeks to recover the state’s climate-related costs—including infrastructure damage, public health impacts, and other social harms—dating back to 1995. The move has inspired similar legislative efforts in states like New York, Maryland, and California. As of mid-2025, Vermont is still in the implementation phase, developing a damages assessment, while facing a legal challenge from the fossil fuel industry aiming to block the law before enforcement begins.

Regulatory risks: Regulators globally are increasingly holding high-emitting companies accountable for both climate and human rights impacts. Governments are implementing carbon pricing mechanisms and stricter emissions standards, which increase operational costs for high emitting industries. Further, the EU’s Corporate Sustainability Due Diligence Directive requires large firms to identify and mitigate adverse environmental and human rights impacts across their value chains and expects companies to transition their operations and value chains to a net zero economy in a rights-respecting way. (Note: As of publication, the existing text has been suspended pending a renewed legislative process that is expected to introduce some revisions.)

Business continuity risks: Companies that fail to address their contribution to climate change contribute to systemic risks with material, economy-wide implications for business continuity. For example:

operational disruptions from extreme heat and declining worker productivity—estimated to fall 2–3% for every degree Celsius above 20°C, affecting billions of workers worldwide (e.g., in agricultural, construction, and manufacturing sectors).

In June 2023, the UN Working Group on the issue of human rights and transnational corporations and other business enterprises issued an information note on the UNGPs and climate change. In reference to the human rights instruments identified in UN Guiding Principle 12, the Commentary on Principle 12, the widely recognized right to a clean, healthy and sustainable environment, and the understanding that anthropogenic GHG emissions are known to cause foreseeable and severe human rights impacts, the working group states that “States and business enterprises have obligations and responsibilities with respect to climate change, and with respect to the impacts of climate change on human rights.”

According to the Working Group, “The obligations of States under the Guiding Principles to protect against human rights impacts arising from business activities includes the duty to protect against foreseeable impacts related to climate change.”

With respect to business enterprises, the Working Group confirms that the responsibilities of those enterprises “under the Guiding Principles to respect human rights and not to cause, contribute to or be directly linked to human rights impacts arising from business activities, include the responsibility to act in regard to actual and potential impacts related to climate change.”

As physical climate impacts are primarily the result of cumulative, global GHG emissions, it may be difficult to establish that any one company has caused a particular, location-specific climate-related harm (e.g., that one company’s GHG emissions in Australia are directly responsible for an extreme weather event in India). However, where a company makes a substantial contribution to cumulative GHG emissions, because their business model substantially relies upon them doing so, that company can be said to have contributed to climate harm, thus requiring the company to “take the necessary steps to cease or prevent its contribution and use its leverage to mitigate any remaining impact to the greatest extent possible”. This supports the expectation that companies with this business model feature should develop and implement robust, credible and Paris-aligned climate transition plans that respect the rights of workers and communities, as well as use their leverage toward achieving broader systemic transition.

Corporations can also be linked to the human rights impacts associated with climate change through their business relationships. Examples of such linkage include a retailer sourcing from a supplier whose operations are carbon intensive, without any indication that the supplier will reduce them; or an investment fund holding equity in a fossil fuel company that has no discernible strategy to reduce its contributions to climate change.

Possible contributions to the Sustainable Development Goals (SDGs)

Addressing impacts on people associated with this red flag can contribute to a range of SDGs depending on the impact concerned, but the most obvious and notable is:

SDG 13: Take urgent action to combat climate change and its impacts

Taking Action

Due Diligence Lines of Inquiry

Are we developing or have we published a robust, credible and science-based climate action strategy or transition plan that recognizes and addresses impacts on workers and communities arising from climate action?

How are we engaging our own workforce, our value chain workers, affected local communities and consumers/end-users in discussions about potential or actual action to address climate change impacts?

How are we evolving our governance, strategy, risk management and metrics/targets to ensure alignment with the objectives of the Paris agreement? How have we integrated potential impacts on people evolving from that evolution?

Recognizing both the consequences for the climate and for people’s human rights of GHG emissions:

Do we: undertake a robust analysis and disclosure of our contribution to global GHG emissions, including the following?

Identifying all our Scope 1, 2 and 3 GHG emissions throughout all our operations, with such identification being science-based, verifiable and informed by input from experts

Identifying hotspots across our operations and value chains

Disclosing climate-related information through recognized frameworks, such as GRI, CDP, TCFD, ESRS E1, or IFRS S2

Do we set ambitious, transparent and verifiable climate-related targets, including:

GHG emissions reduction targets across Scopes 1, 2 and 3 emissions

Transition-specific alignment targets that directly reflect our company’s progress on critical decarbonization milestones within our sector

Do we disclose the details of how our capital expenditure plan aligns with our climate action and human rights objectives?

Have we undertaken scenario analysis to assess resilience of the company’s operations and value chains, as well as the people its operations and value chains may impact, under various warming pathways (e.g., 1.5°C or 4°C)?

How do we ensure that our public affairs and policy advocacy activities are aligned with the objectives of our climate and human rights actions?

Do we rely on land-based carbon dioxide removals or the use of carbon credits to meet our GHG emissions reduction targets? If so, do we have mechanisms in place to evaluate the social and environmental integrity of doing so?

How do we assess whether our climate-related strategies and plans could impact stakeholder groups, namely, our own workers, workers in the value chain, communities and end users, with a particular focus on vulnerable populations?

Mitigation Examples

For companies whose business models substantially rely upon high emitting activities, products or services, examples of integrated, ambitious, organization-wide, and Paris-aligned action is not yet common. However, there are examples of companies that are making important, if partial, strides to address their contribution to climate impacts. For example:

Large agrifood companies, such as Danone, Mars, Nestlé and PepsiCo, have acknowledged that, given the realities of the climate challenge within their sector, GHG emissions reduction targets are necessary but not sufficient. These companies have also set no-deforestation commitments for some or all high-risk commodities where deforestation is most prevalent. According to the 2025Corporate Climate Responsibility Monitor, “these examples demonstrate how transition-specific alignment targets can complement emission reduction targets to guide sector-specific corporate transitions”.

Decision-useful climate disclosures that address the Just Transition:

Scottish and Southern Energy (SSE) in the UK has publicly disclosed its Just Transition strategy, which considers the impact its transition plan has on people.

Collaborative initiatives that use leverage to affect change:

Climate Action 100+ is an investor-led initiative composed of around 700 investors globally and responsible for over USD 68 trillion in assets under management, which aims to ensure the world’s largest corporate greenhouse gas emitters take action on climate change.

Alternative Models

Orsted, the Danish energy company, was once one of the highest emitting energy companies in Europe, due to its coal-fired power and its oil and gas assets. Since 2009 it has undergone a transition to become a global leader in renewable energy, reducing its GHG emissions by 98% (from 2006 levels, scope 1 & 2 only) and aims to be net zero GHG emissions across its value chain (scope 3) by 2040. The company also continues to use its leverage in support of broader systemic transition, in the context of collaborative initiatives, as well as in advocating for the global elimination of fossil fuel subsidies. While there are concerns about the company’s transition strategy, including its 2017 oil and gas divestment (rather than gradual and actively managed decommissioning), this is one of very few examples of a high emitter’s strategic reorientation, with important lessons for other transitioning or soon-to-be transitioning companies.

In Australia, where the market for “carbon neutral cattle” is growing, farmers are experimenting with carbon neutral cattle systems focused on soil carbon sequestration to offset greenhouse gas emissions, aiming for net-zero emissions from cattle birth to sale.

In response to foreign competitive pressures Sweden has developed expertise in niche environmentally friendly steel products and is developing fossil fuel free steel. Such technological innovation is seen as essential to maintaining Swedish competitiveness in the sector.

Citation of research papers and other resources does not constitute an endorsement by Shift of their conclusions.

This website uses cookies to improve your experience. We'll assume you're OK with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.